Whether a married spouse can bind the community property of both spouses with just their signature is controlled by the law of the state in which the spouses reside. In Alaska, Arizona, Idaho, Louisiana, Nevada, New Mexico, Washington, and Wisconsin, the community property laws of each state require that the spouse of the guarantor must CONSENT to the other spouse’s guaranty to bind the community property of both spouses. In the remainder of the community property states a single spouse can bind the community property of both spouses.

Our previous coding logic looked to the state in which the collateral real property was located to determine whether spousal consent was necessary for the guaranty since, for most transactions, the guarantor resided in the state where the real property was located. More precise coding requires an understanding of the state of residency of the guarantor and their spouse to provide a much more definitive determination of which state’s community property rules should apply.

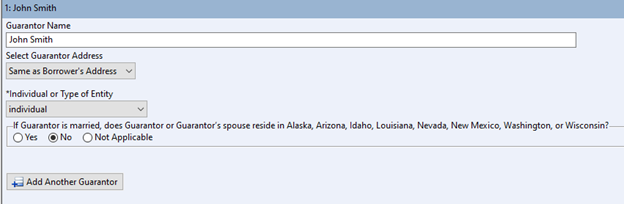

We implemented these changes in our most recent update to the Lightning Docs server. Specifically, in the interview dialogue, you will see new questions as they relate to the Guarantor:

Here you will need to identify if both (a) the Guarantor is married, and (b) they or their spouse are a resident of the states mentioned above. If the answer is No, or Not Applicable then no spousal consent will populate in the Loan Documents. If the answer is “Yes” then a spousal consent will populate.

A spousal consent does not make the consenting party an additional Guarantor to the Guaranty. Instead, it only acknowledges the non-guarantor spouse’s consent to bind the entire community property estate of both spouses.

For example, John Smith and Jane Smith are married, residents of Arizona and only Jane Smith signs a Guaranty to which John Smith consents, if the loan defaults, the lender can file a breach of guaranty action only against Jane Smith. However, if a judgment is obtained against Jane Smith, all of (a) Jane Smith’s personal property assets, and (b) Jane and John Smith’s community property assets would be subject to judgment since John Smith consented to the Guaranty. The lender would have no recourse against John Smith’s personal property assets. If John Smith did not consent to the Guaranty, then the lender would only have recourse against Jane Smith’s personal property assets and ½ of the community property assets held by Jane and John Smith.

For any questions about this update, please connect with our team at Lightning Docs by sending an e-mail to team@lightningdocs.com.